Business Advice

The Latest Tax Changes for the E-commerce Industry

The world of e-commerce is booming, and with it comes many tax rules that businesses in this space must contend with. Keeping up with these

We provide expert tax advice, personalized services and innovative tax solutions for your business. Whether it’s a quick consultation or a longer-term project, we can assist you with:

We offer you partnerships with knowledgeable CPAs to help you resolve your tax issues, so that you can focus on your core business. Fusion CPA uses an in-house cloud-based network to minimize your costs and maximize our service.

In addition, we offer specialized expertise for a variety of needs:

Tax compliance requires accurate record-keeping, a knowledge of tax laws, and a tax return that is completed correctly.

While automated services might be convenient, they won’t offer you the thorough tax planning and preparation that a CPA can. At Fusion CPA, our dedicated staff use accounting software and industry knowledge to streamline your taxes, from start to finish.

Because we offer outsourced tax services, you only pay for the help you require! You can contact our client success team to discuss your needs.

This refers to the period in which tax returns must be sent to the IRS. For individual taxpayers, the tax year is the same as the calendar year, which means that it starts on January 1 and culminates on December 31.

Taxes are filed for the previous year, and the filing deadline is April 15. However, if you have filed an extension, your tax return is due by October 15.

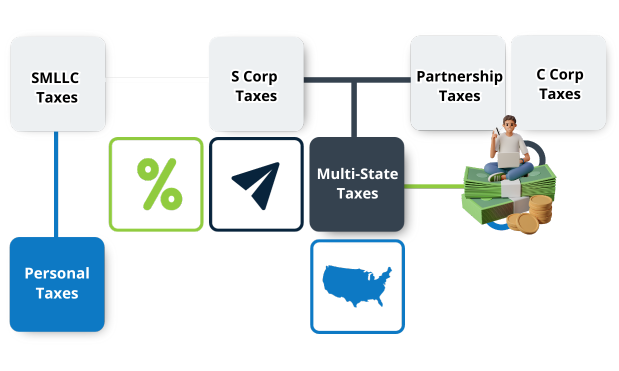

Business tax returns for partnerships and S Corporations are due on March 15. C Corporation returns are due on April 15, if their fiscal year is the same as the calendar year. Single member limited liability companies (SMLLCs) taxes are typically filed with the owner’s personal tax return on April 15, or October 15 if an extension was filed.

Our extensive article on corporate tax deadlines provides further insights.

You can view your refund on the federal government’s website set up for this purpose. Our clients can simply contact our office for the status of their refunds.

Tax calculations in the United States are notoriously complex. American taxation is progressive, which means that tax assessment levels increase along with the income you report. Tax rates range between 10% and 37%, depending on your filing status.

Thereafter, your income and qualified deductions are determined, resulting in the calculation of taxable income. However, there are a number of other factors that need to be taken into account to determine your overall tax liability. Our CPAs can guide you through this complicated process.

Income from C Corporations is currently taxed at 21%. S Corporations and partnerships are “flow through” entities that are not subject to Federal tax. Like individual taxpayers, SMLLCs are taxed between 10% and 37% on their income.

The tax calculation process is different for business entities. It considers extra factors, like equipment, depreciation, and payroll. Nonetheless, the determination of taxable income is always crucial to tax calculations. Learn more in our article about US corporate tax rates.

There are several entity structures that businesses can choose from. Selecting the best option depends on different factors, including your business size, preferred tax structure, and more. As such, each entity comes with its advantages and drawbacks.

Fusion CPA can help you choose the structure that best suits your needs.

Self-employment or freelance income is reported on Schedule C of your tax return. Moreover, these individuals need to make quarterly estimated payments. In this case, the tax year is divided into four payments periods:

Self-employed individuals can benefit from a number of tax deductions, such as the home office tax deduction. However, in order to do so, you must keep detailed records of qualifying expenses.

Tax deductions and credits both translate to more money in your pocket. The only difference is deductions reduce your taxable income, and credits reduce your tax liability.

Tax deductions refer to expenses typically seen as necessary for business or individual earnings. As such, they lower the amount of income that is subject to taxation.

Tax credits incentivize specific behaviors or activities that the government deems beneficial to individuals, businesses, or society as a whole. For example, education expenses or renewable energy technologies. These credits provide a dollar-for-dollar reduction in your tax liability.

Estimated taxes are periodic payments made by those who receive income that is not subject to withholding. This includes self-employed individuals, freelancers, and those with significant investment income.

Essentially, estimated taxes are your calculation of what to pay the IRS. Form 1040-ES is used to do this. Estimated payments can be done in four payments periods:

It’s important to consult your CPA to ensure accurate submissions.

Capital gains tax is paid for profits made from selling an asset, often in addition to paying corporate income taxes.

Investment income and capital gains are reported on Schedule D of Form 1040. The exact tax rate depends on factors such as your income and how long you have held the investment. These rates can be 0%, 15% or 20%, based on various factors.

To determine which rate applies to you, speak to one of our tax professionals.

There are potential tax benefits and implications for both scenarios. One of the primary benefits of buying a home is the mortgage interest deduction. Here, the interest paid on your mortgage can be deducted from your taxable income. However, selling a home could lead to capital gains taxes if your profits exceed the exclusion limits.

For further guidance, consult with our tax advisors.

Traditional IRAs are tax-deferred, meaning that you don’t have to pay tax on any interest until you withdraw the money, at which point they are taxed at an ordinary income rate. However, depending on the type of retirement account you have, the contributions you make may allow for a tax deduction each year.

Partner with Fusion CPA to avoid common tax mistakes for retirees.

Moving to a new state can be intricate to navigate, as different states have varying tax rates and rules. You may need to file part-year resident returns in both states, which can be challenging if you are not familiar with tax residency rules per state.

Profits from selling stocks or bonds are subject to capital gains tax. Gains from selling section 1202 qualified small business stock are taxed at a maximum rate of 28%. Despite this, the tax rate depends on factors such as your income and how long you have held your stocks or bonds.

A tax expert can offer you personalized advice.

These are reported on Schedule E of your tax return. While it is possible to deduct rental-related expenses, such as repairs and maintenance, you must have detailed records of these expenses as evidence.

Yes. Charitable donations are deductible and must be claimed as itemized deductions on Schedule A of Form 1040. For tax years 2023 and 2024, the limit on charitable cash contributions is 60% of your gross income. You must keep records of your contributions in order to claim them as deductions on your tax return.

Yes. You can qualify for a credit of up to $7,500 under Internal Revenue Code Section 30D if you buy a new, qualified plug-in EV or fuel-cell electric vehicle (FCV). The credit is available to individuals and businesses, but is subject to qualifying criteria.

Tax Benefits | Tax Filing | How to fill out Form 1120-S | Estimated Taxes

Let us assist this tax seasonPartnership Tax Filing and Deadlines | Self-Employed Taxes | Estimated Taxes | Form 1065

Keep readingTax Benefits | Tax Filing | How to fill out Form 1120-S | Estimated Taxes

Let us assist with seamless migrationSingle-Member Limited Liability Company Taxes | Estimated Taxes | Tax Returns

Tax Benefits | Foreign Earned Income Exclusion (FEIE) | Foreign Tax Credit (FTC)

Work with international experts

The world of e-commerce is booming, and with it comes many tax rules that businesses in this space must contend with. Keeping up with these

By leveraging the power of QuickBooks Plus, you can maximize your tax deductions, streamline your accounting processes, and stay in control of your business finances.

If you moved before the Tax Cuts and Jobs Act which came into effect in 2017, you may be able to deduct moving expenses if the move was for work or business purposes.

Join our client journey without the commitment of an in-house accountant, tax or finance team!

Our team will address any accounting clean-up tasks that need to be executed and analyze your accounting ecosystem for optimization opportunities and to stabilize your business.

We analyze your accounting to see where you can save with strategic tax planning. We don’t just put out the fire, but also streamline your tax deductions.

We’ve had great success with the business management system, and we love providing our clients with CFO advisory to reach their unique goals.

Disclaimer: This page is not intended to be the rendering of legal, accounting, tax advice, or other professional services. Articles are based on current or proposed tax rules at the time they are written, and older posts are not updated for tax rule changes. We expressly disclaim all liability in regard to actions taken or not taken based on the contents of this blog as well as the use or interpretation of this information. Information provided on this website is not all-inclusive and such information should not be relied upon as being all-inclusive.