This will depend on your tax nexus. A nexus is created when your business has a connection to or presence in a state or jurisdiction, such as a physical presence or economic activity, which triggers a tax collection obligation. Note that the exact definition of nexus may vary across states, so it’s best to consult with your CPA to see whether you need to file multi-state taxes.

Yes, spouses can file taxes in different states, usually if they live apart for work, have separate residences, or if one or both have income from different states.

What are the tax considerations when doing business in another state?

Expanding into another state can improve your bottom line and boost your business growth. Moreover, since some states have lower taxes, this can be beneficial for employees earning outside their resident state.

Our comprehensive services offer you peace of mind when expanding into other states. With specialist knowledge of multi-state expansion, we are uniquely positioned to help you take advantage of available tax benefits.

For businesses: Different states have different business climates, tax consequences and federal filing requirements. Addressing these challenges early in the expansion process can help your business avoid penalties for late filings and underpaid taxes.

For individuals: In the United States, many individuals move to lower-tax states in the hopes of saving money. Similarly, with the rise in remote work, it’s possible to be employed in a state different from your residence state. However, if this is not handled correctly, it could lead to double taxation, as each state has varying tax requirements.

Our CPAs can help you navigate multi-state taxes successfully.

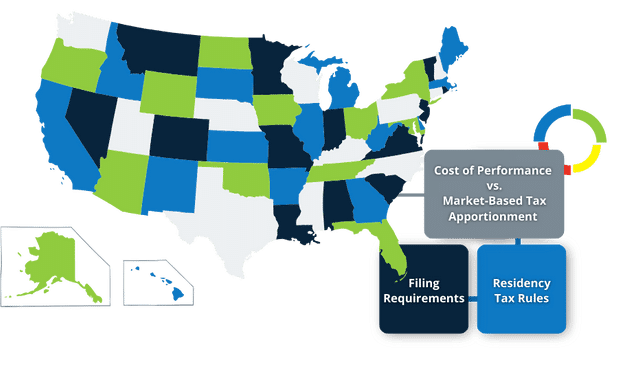

When your business operates in states other than the one in which it is incorporated, it may influence your state and local taxes. Apportionment allows you to establish the percentage of profits subject to the tax laws of the different states within which you operate. This is calculated using a formula which considers your business’ sales, property, or payroll. The main apportionment methods are cost of performance and market-based tax apportionment.

Under the cost of performance method, income is allocated to the state where the cost of performing the service is greatest. Market-based apportionment allocates income to the state in which your market or customer is located, instead of where any costs are incurred.

Any income which cannot be apportioned according to the standard apportionment formula is allocated to a particular state.

Both apportionment and allocation aim to prevent double taxation of income, by ensuring that each state can tax its fair share of your business’ income based on activities within that state.

It’s worth noting that the specific rules and methods used for apportionment and allocation may vary across states. This makes multi-state tax compliance complex for businesses operating across state lines.

Running a business across state lines has different tax obligations and benefits. These include considerations around lower tax rates, being recognized as a resident of the new state, and exemption of home state tax obligations.

Owning property in multiple states and traveling between states can also impact your tax liability. Most states have a threshold for the number of days you’re allowed to stay in the state without being liable for taxes. If you frequently travel between states, it is important to track the number of days you’ve spent in each state. This can help you ensure accurate tax submissions and maximize potential benefits. There is software available to help you with this.

Software that can help you track your residency days per state

Multi-State Taxes

Here, you will find more information about tax business climates and requirements for particular states.

Our team will address any accounting clean-up tasks that need to be executed and analyze your accounting ecosystem for optimization opportunities and to stabilize your business.

We analyze your accounting to see where you can save with strategic tax planning. We don’t just put out the fire, but also streamline your tax deductions.

We’ve had great success with the business management system, and we love providing our clients with CFO advisory to reach their unique goals.

Disclaimer: This page is not intended to be the rendering of legal, accounting, tax advice, or other professional services. Articles are based on current or proposed tax rules at the time they are written, and older posts are not updated for tax rule changes. We expressly disclaim all liability in regard to actions taken or not taken based on the contents of this blog as well as the use or interpretation of this information. Information provided on this website is not all-inclusive and such information should not be relied upon as being all-inclusive.