Every industry has its accounting difficulties, and the e-commerce industry easily leads the charge when it comes to bookkeeping challenges, which oftentimes can be a lot more complicated than other industries. Learn more about the accounting challenges to be aware of when running an e-commerce business.

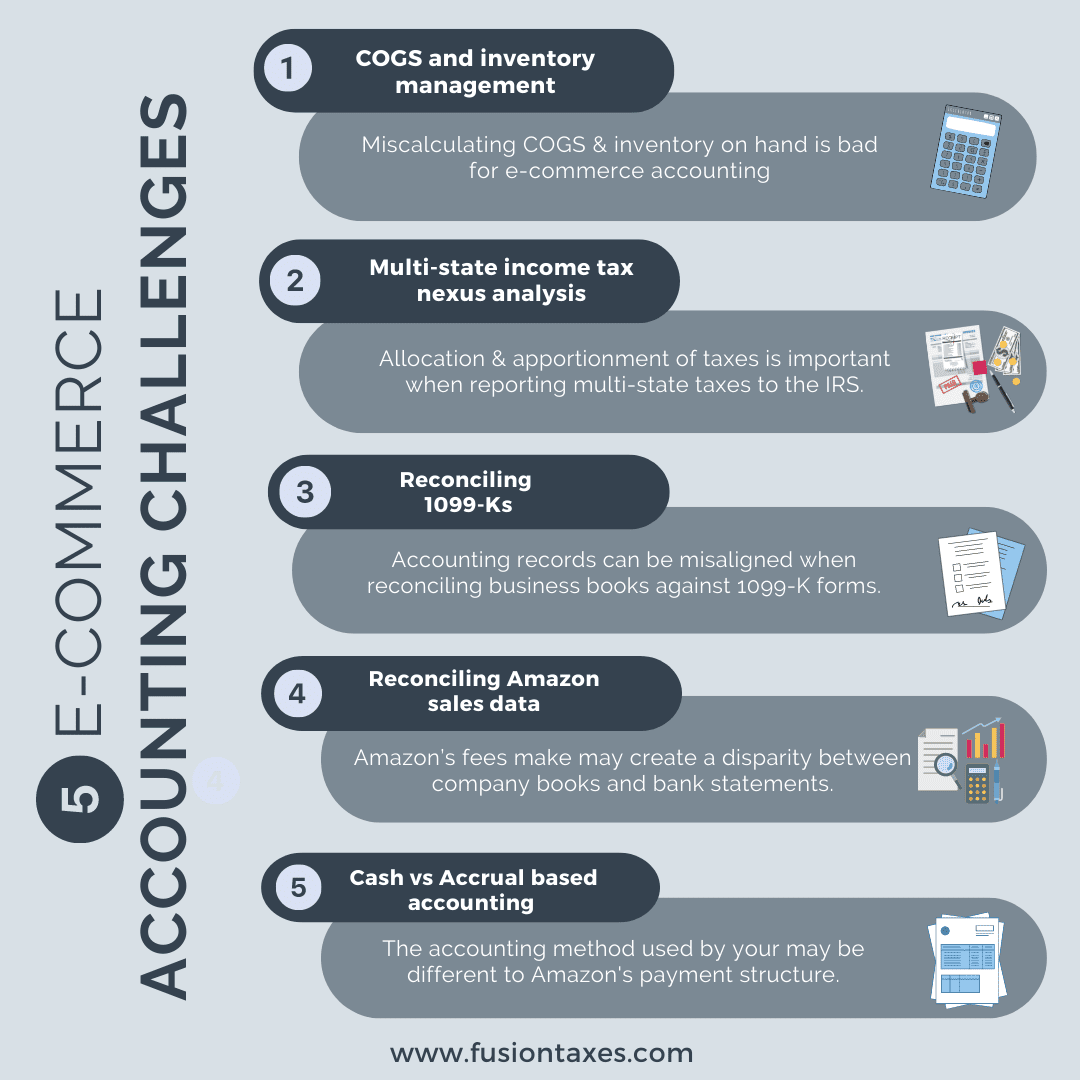

1. COGS and inventory management

Cost of goods sold (COGS) is one of the most important aspects of accounting, it takes into account all of the direct costs involved in the process of selling products, to establish the actual cost of doing business as an e-commerce retailer. Understanding the COGS gives retailers a clearer understanding of their profits and how to manage their cash flow. It also directly affects accounting management and tax calculations.

The following basic COGS formula can be used for e-commerce businesses:

Direct costs involved in e-commerce inventory can include: raw materials and/or manufacturing costs as well as packaging costs and distribution or shipping costs.

Simply estimating the COGS can have devastating effects on the books of e-commerce traders.

Similarly to the miscalculation of COGS is the challenge of accurately understanding of inventory on hand and how to account for it. Knowing how much inventory your business actually has on hand can be challenging when having to take into account the amount of stock in production vs the number in a shopping cart, on its way to clients, or making its way back to your warehouses as returns. It is not uncommon for e-commerce retailers to have thousands of dollars worth of inventory unaccounted for. Yet, knowing the inventory numbers greatly affects your accounting. This is why it is of utmost importance that e-commerce businesses get the correct inventory management software setup as the GAAP matching principle requires that revenues and any related expenses be recognized together in the same reporting period, which might become challenging when considering the inventory challenges outlined above. NetSuite’s inventory management software set up by a CPA that understands the intricacies of your specific e-commerce business might help mitigate some of the challenges around stock within your e-commerce business.

2. Multi-state income tax nexus analysis

E-commerce provides businesses with access to much larger markets, and the correct infrastructure makes it easy to sell to markets in other states. While this can rapidly boost sales, there is a lot to consider from a tax and accounting perspective, especially when dealing with multi-state sales. Keeping track of the tax laws that apply to sales per state, can be confusing, and getting the allocation and apportionment right when reporting to the IRS requires the expertise of a CPA that understands multi-state taxes. This is especially important to avoid double taxation – in the state you are headquartered and in the multiple states within which your e-commerce business operates.

3. Reconciling 1099-Ks

Form 1099-K is used to report third-party network payments via credit/debit card transactions. The form requires credit card companies, and third-party processors, to report the payment transactions they process for businesses. This means that each of the payment processes your e-commerce business makes use of to process sales will summarize your transactions. The challenge for many e-commerce businesses is that they would have to reconcile their personal accounting books against the 1099-K forms, in which payment processors would have reported their sales. This can become difficult when records don’t match and transactions are misaligned. Not only will this have a ripple effect on the bookkeeping of your business, but if not handled correctly, can lead to penalties with the IRS. It is advisable for e-commerce businesses to partner with a CPA that understands third-party reporting and tax filing for e-commerce businesses.

4. Reconciling Amazon sales data

Similarly to 1099-K’s, keeping financial statements accurate and up-to-date might be a challenge for Amazon sellers. This is largely due to Amazon’s reserved balances, in which the platform holds a percentage of your sales revenue as insurance against damages or refunds; and the fact that the money paid into your business account by Amazon would be the amount due to you after Amazon deducted their reserved balance and commission fees, may create a disparity between the company bookkeeping and bank reconciliation statements. It is important for the CPA setting up your accounting software to make provision for these in the recordkeeping to make tax filing less laborsome for your e-commerce business.

5. Cash vs Accrual based accounting

The accounting method used by your e-commerce business may also clash with the payment structure by Amazon. This would be especially evident in the recon statements for businesses that make use of cash-based accounting, in which sales are reported immediately, despite when the funds reflect in the account. This would mean that your business reports the sale in its books when it took place (in January, for example), while Amazon only processes that payment to the business a few weeks later, creating a potential misalignment in the recon statement. A professional CPA would know how to set up your accounting processes in a way that minimizes these accounting inconsistencies.

At Fusion, our CPAs are trained to set up accounting software to best serve the needs of your e-commerce business and help you keep books clean for a smoother tax filing process. Contact us to discuss the best accounting approach for your e-commerce business.

View this article at a glance, here:

__________________________________________________________

This blog article is not intended to be the rendering of legal, accounting, tax advice or other professional services. Articles are based on current or proposed tax rules at the time they are written and older posts are not updated for tax rule changes. We expressly disclaim all liability in regard to actions taken or not taken based on the contents of this blog as well as the use or interpretation of this information. Information provided on this website is not all-inclusive and such information should not be relied upon as being all-inclusive.