When individuals and entrepreneurs are in the early planning stage of moving to a state with no income tax liabilities or a low-income tax, due diligence is the starting point. While states with no imposed state income tax or a lower state income tax may be attractive for entities or retirees, there are factors to consider. Of course, it can be confusing to believe that the move can reduce your income tax liabilities to save money, which is misleading. States have to generate revenue, whether it is through sales & excises, property, and individual income tax for funding schools, roads, streets, and in-state infrastructure. If you continue reading this guide, you can learn more about US states with no-income or low-income taxes, the peripheral implications, and the evaluation process.

Factors to Consider Before You Move to a State With No or Low Income Taxes

Before entrepreneurs or retirees decide to move from higher-tax states, they must consider possible state-exit implications, including:

- The sale of property.

- Withdrawals from retirement funds.

- Cashing out investments.

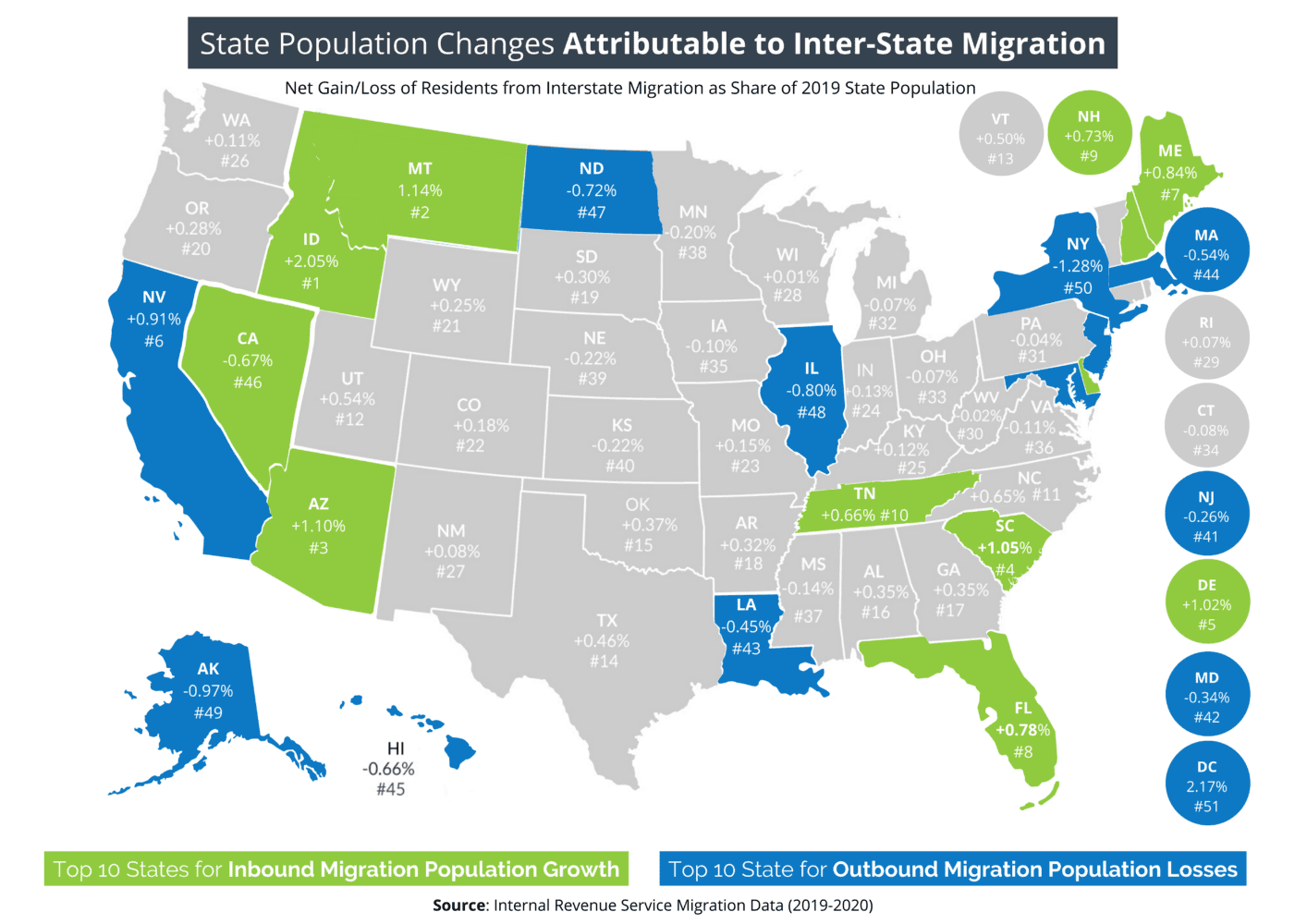

In 2022, the Tax Foundation Organization listed seven states in the United States with a no-income-tax structure. Texas, Tennessee, South Dakota, Florida, Alaska, Florida, and Nevada are on the list with no individual income taxes but impose property, sales & excise taxes. Retirees can avoid state taxes when living in those states on social security benefits, pensions, and other retirement income sources. Besides individual income tax, some individuals may not consider the property and sales taxes when moving to a state with low-income tax. Investigate all state and local taxes, such as death and property, before moving to another state and estimate how much taxes you might have to pay.

How to Evaluate States Before Migrating

It is necessary to do thorough due diligence if you are planning to move to another state to retire and settle until death. Some states with no or lower individual income taxes may have higher property taxes and an estate or inheritance tax. A state may charge an estate tax against an entire taxable property, regardless of the ownership, and an inheritance tax against inheritances received by particular beneficiaries. In Kentucky, for example, there is no estate tax but an inheritance tax ranging from four percent to 16 percent. Another example is Maine which that the top estate tax rate at 12 percent and an exemption allowance of $5.8 million for 2020. Vermont, Rhode Island, Oregon, New York, Minnesota, Massachusetts, and the District of Columbia have a tax rate of 16 percent, at the time of publishing this article.

While Washington State has no individual state income tax, it has an estate tax that could be costly in the event of death. It is one important reason you should be cautious when moving to a state with no income tax or low-income taxes. When you consider combining state and local sales tax rates, the total percentage rate can reach over 10 percent. If you are about to move to Florida to retire, it is a non-taxable income state with no death tax and low sales taxes in various jurisdictions. Examine your situation by considering all taxes, including sales, property, death, and state income migrating to another state.

Retirement Income Tax Considerations

Once you start receiving social security benefits or pension income from a traditional IRA or 401K after retirement, you must pay taxes. You will need to pay federal income taxes and taxes on parts of your social security income at the end of each year. Factors to consider in determining whether you pay taxes on the income are most likely the total retirement payments. The tax you pay each year on income will factor in your household’s total retirement income you and your spouse receive and filing a joint or separate tax return.

Check the state’s taxation rules on pension income because some states tax pension money while others do not influence people to consider moving for retirement. States can not tax pension money you earned within their jurisdictions if you move your legal resident to another state. Moving to a state with no income tax, such as Florida, you may not be liable for any income tax on the pension to the state you move from and receive income from your former employer.

With a traditional IRA, you will owe taxes on the earnings at your standard income tax rate when withdrawn. A Roth IRA differs, with no tax on earnings, when you receive funds and follow specific rules and guidelines. One strict rule requirement is to have the Roth IRA account for five years or longer before qualifying for your earnings and interest to become tax-free. If you are moving states during 2022, you will have to pay income tax to each state based on the amount you earned and where you are filing your tax return.

The best suggestion is to perform due diligence before moving to a state with a low-income tax or no income on your earnings. Research how the migration will affect you financially and your tax liabilities, including property income (federal and state) and sales. Consider consulting with a CPA who can evaluate and assess your asset profile to determine how you might be holistically taxed when exiting a state to live in another.

Fusion CPAs help individuals and entities accomplish successful moves to other states in the US by offering financial planning, tax preparation, bookkeeping, and software solutions. Trying to escape a state with high-income taxes could come with other hidden costs and must be carefully considered. With our outsourced accounting and tax services, you will know the economic outcome, tax considerations & implications, and your financial position before moving to a state with no income tax.

_______________________________________________________

This blog article is not intended to be the rendering of legal, accounting, tax advice or other professional services. Articles are based on current or proposed tax rules at the time they are written and older posts are not updated for tax rule changes. We expressly disclaim all liability in regard to actions taken or not taken based on the contents of this blog as well as the use or interpretation of this information. Information provided on this website is not all-inclusive and such information should not be relied upon as being all-inclusive.