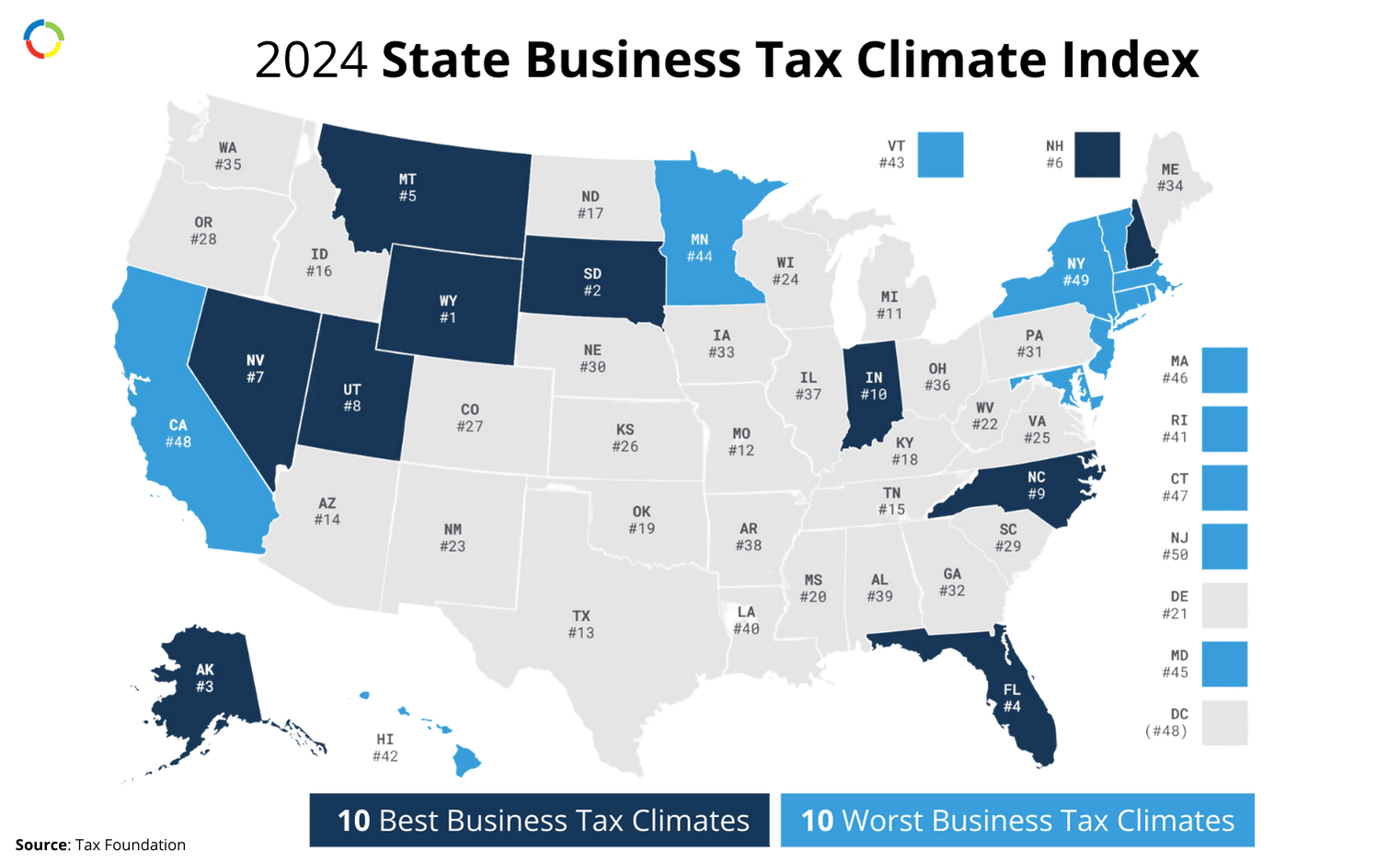

Tennessee has a favorable corporate tax environment, with a 6.5% corporate income tax rate, and no individual income tax.

Understanding the cost of apportionment in the state can help you to accurately report your earnings to the IRS and your local government.

Corporations

- Filing Requirements. Generally, if you conduct business within a county and/or incorporated municipality in Tennessee, you must register for and remit business tax. But remember that corporate tax consists of two separate components: state business tax, and city business tax.

With a few exceptions, all businesses that sell goods or services must pay state business tax. This includes companies that are physically located in the state, as well as those active but not present in the state. Out-of-state businesses must pay the state business tax if you have a substantial nexus in Tennessee.

- Allocation and Apportionment. Tennessee follows the market-based rule in sourcing receipts from performance of services to the state.

Partnerships

Filing Requirements. Tennessee does not impose excise taxes on partnerships.

Employees & individual filers

Tennessee does not tax an individual’s earned income. This means that don’t need to file a personal tax return in the state. However, if you earn income or have other tax obligations in other states, you’ll still need to file returns in those jurisdictions. Also note that while Tennessee does not tax your earned income, you are still subject to federal income tax. As such, you still need to comply with federal filing requirements.

Ensuring Accurate Tax Filings

To keep a handle on different laws and tax implications, consult an expert CPA.

Fusion CPA has a team of certified public accountants that are highly skilled in handling multi-state taxes. We’re can help you to take the stress out of tax season, so that you can focus on what really matters. To see how we can help you with a proactive tax strategy to save you time and money, schedule a Discovery Call with one of our CPAs.

To see how we can help you with a proactive tax strategy to save you time and money, schedule a Discovery Call with one of our CPAs.

____________________________________________________

This blog article is not intended to be the rendering of legal, accounting, tax advice, or other professional services. Articles are based on current or proposed tax rules at the time they are written. Older posts are not updated for tax rule changes. We expressly disclaim all liability in regard to actions taken or not taken based on the contents of this blog as well as the use or interpretation of this information. Information provided on this website is not all-inclusive and such information should not be relied upon as being all-inclusive.