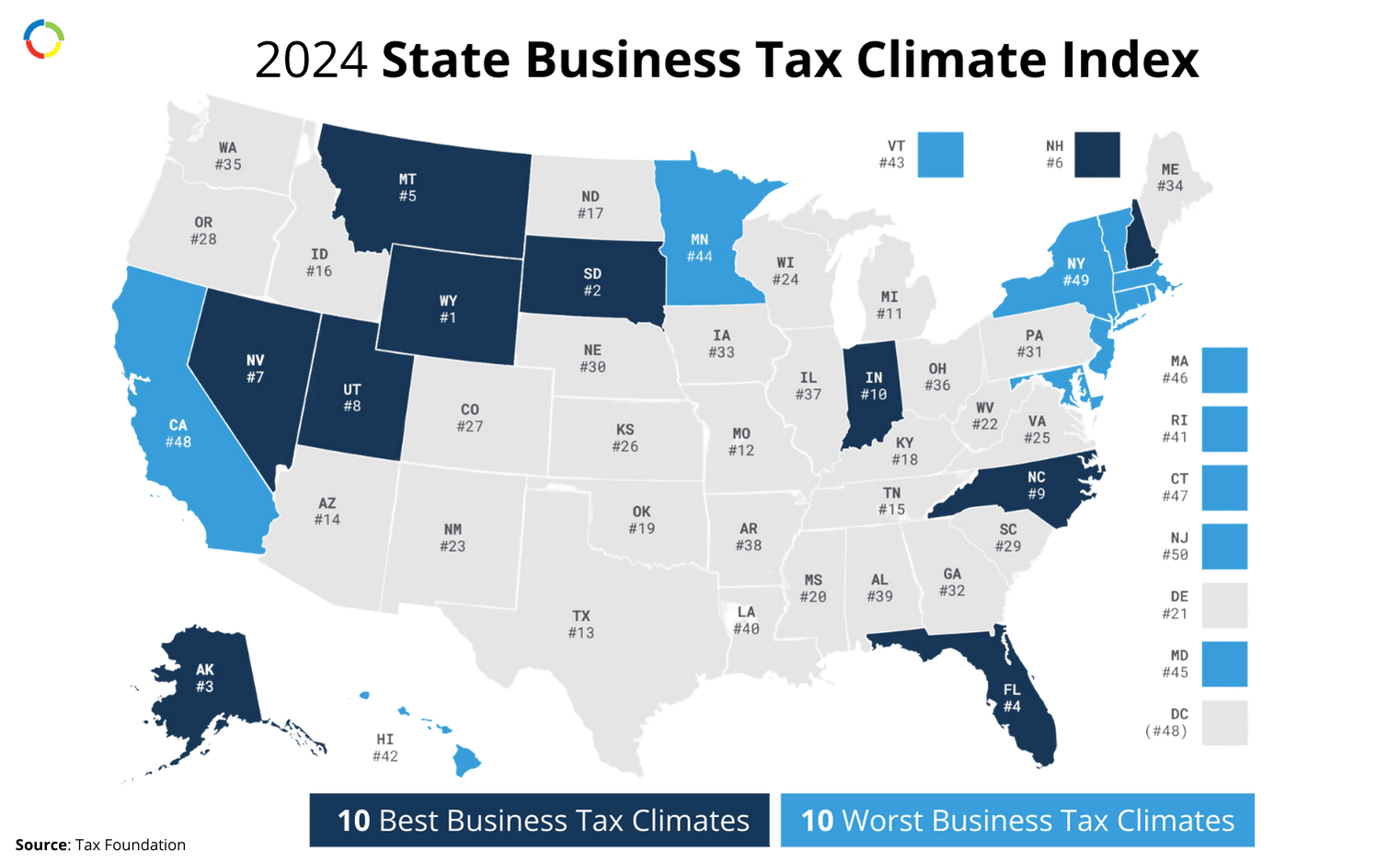

New York has variable tax rates. The individual income tax rate ranges from 4% to 10.9%, while corporate rates range between 6.5% and 7.25%. Entrepreneurs in the state also enjoy a wealth of business development resources.

Corporations

- Filing Requirements. An S corporation is a small business corporation, as permitted under Subchapter S of Chapter One of the Internal Revenue Code (IRC).

Generally, an S corporation does not pay federal income tax. Instead, income and deductions are passed through to shareholders for them to report on their personal income tax returns.

Shareholders of federal S corporations subject to Tax Law Article 9-A can make a New York S election. This is done by filing Form CT-6, Election by a Federal S Corporation to be Treated as a New York S Corporation. This includes both corporations organized under New York State law and foreign corporations (those organized under the laws of any other state) that do business, employ capital, own or lease property, maintain an office, or derive receipts from activity, in New York State.

- Allocation & apportionment. New York follows the single receipts factor in sourcing receipts from performance of services to the state.

Partnerships

Filing Requirements: Partnerships are not subject to personal income tax. But every partnership has either:

(1) at least one partner who is an individual, estate, or trust that is a resident of New York State, or

(2) any income, gain, loss, or deduction from New York State sources, must file a return on Form IT-204, regardless of the amount of its income.

Otherwise, state law does not currently require a partnership to file a return solely because it has a partner that is a partnership or corporation, even though the partner may be responsible for filing its own return with New York State.

Employees & individual filers

Generally, you must file a New York State income tax return if you’re a state resident required to file a federal return. To do so, you’ll need to complete Form IT-201. You may also have to file a return if you’re a nonresident with income from New York State sources.

If you moved into or out of New York during the year, you are considered a part-year resident and need to file Form IT-203 to report income received during the period you were a resident.

Ensuring Accurate Tax Filing

Consulting an expert CPA can help you keep a handle on different laws and tax implications.

Fusion CPA has a team of certified public accountants who are highly skilled in handling multi state taxes. We’re positioned to help you take the stress out of tax season, so you can focus on what really matters.

To see how we can help you with a proactive tax strategy to save you time and money, schedule A Discovery Call with one of our CPAs.

The information presented in this blog article is provided for informational purposes only. The information does not constitute legal, accounting, tax advice, or other professional services. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability of the information contained herein. Use the information at your own risk. We disclaim all liability for any actions taken or not taken based on the contents of this blog. The use or interpretation of this information is solely at your discretion. For full guidance, consult with qualified professionals in the relevant fields.