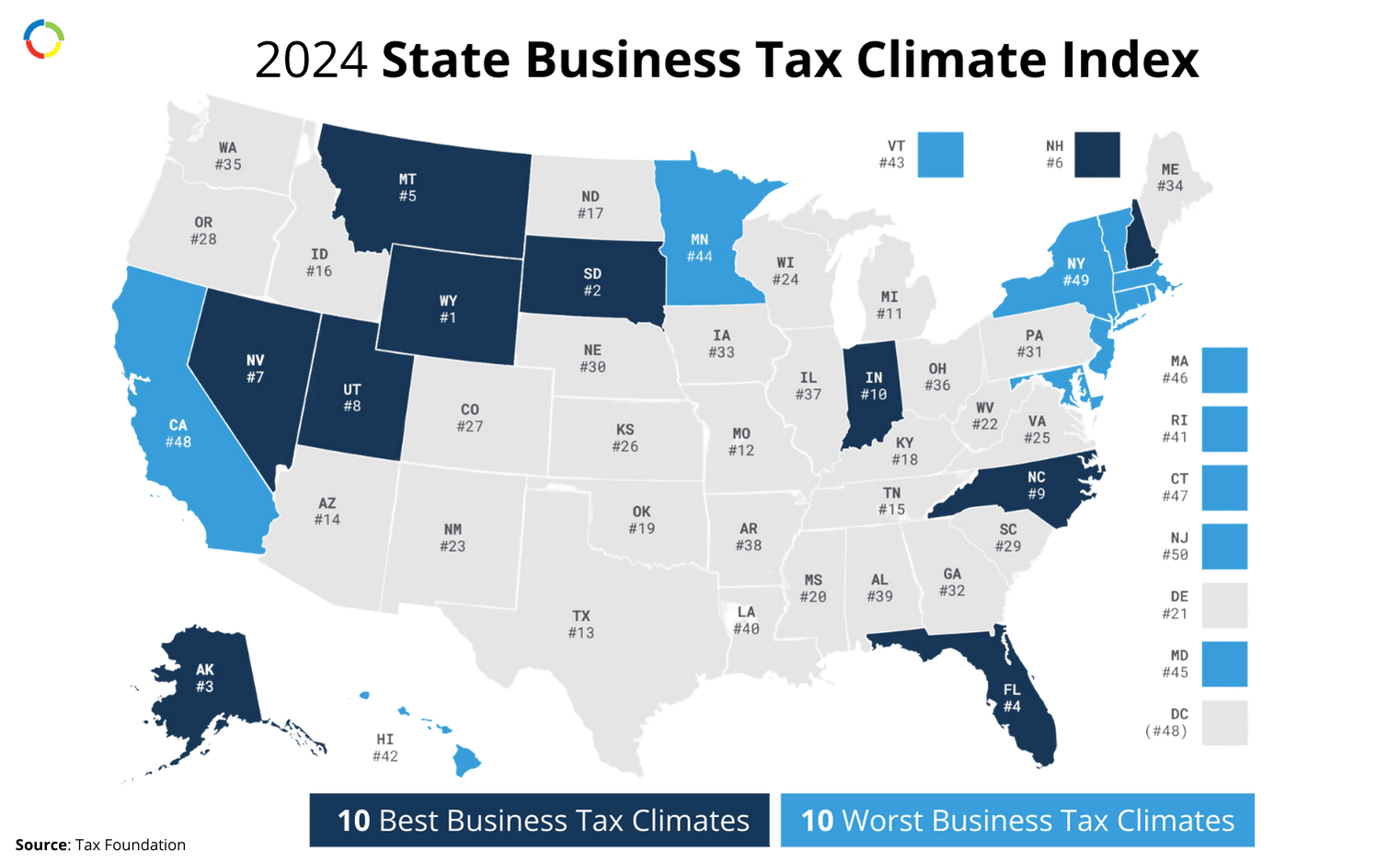

Michigan has a lower cost of living than many other states. It also allows for easy international business access, as it’s located within 500 miles of the US-Canadian border. The state has a 4.25% individual income tax rate, and a 6% corporate income tax rate.

Understanding the cost of apportionment in Michigan can help you accurately report earnings to the IRS and local government.

Corporate Income Tax

- Filing Requirements. The Michigan Corporate Income Tax (CIT) imposes a 6% corporate tax on C corporations and taxpayers taxed as corporations federally. The CIT has one credit, the small business alternative credit, which offers an alternate tax rate of 1.8% of adjusted business income. There are no other credits, except those under the MBT election.

Insurance companies and financial institutions pay alternative taxes. Also, taxpayers with less than $350,000 in gross receipts and/or $100 or less in annual liability don’t need to file or pay CIT. The gross receipts threshold does not apply to financial institutions or insurance companies.

- Allocation & apportionment. Michigan follows the 100% sales factor rule in sourcing receipts from the performance of services to the state.

Employees & individual filers

You must file a state income tax return if you owe tax, are due a refund, or your AGI exceeds your exemption allowance. You should also file a Michigan return if you file a federal return, even if you do not owe state tax.

In Michigan, individuals are required to file a state income tax return for the 2023 tax year (due in 2024) under the following circumstances:

Part-year residents and nonresidents who earned income from Michigan sources must also file a return if their Michigan income exceeds their personal exemption allowance.

Taxpayers with income from Michigan who moved out of or into the state during the year, as well as individuals claiming credits like the Homestead Property Tax Credit or the Home Heating Credit, are also required to file.

Download our Multi-State Tax Filing Requirements Guide

Ensuring Accurate Tax Filing

Consulting an expert CPA can help you keep a handle on different laws and tax implications.

Fusion CPA has a team of certified public accountants who are highly skilled in handling multi state taxes. We’re positioned to help you take the stress out of tax season, so you can focus on what really matters.

To see how we can help you with a proactive tax strategy to save you time and money, schedule A Discovery Call with one of our CPAs.

The information presented in this blog article is provided for informational purposes only. The information does not constitute legal, accounting, tax advice, or other professional services. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability of the information contained herein. Use the information at your own risk. We disclaim all liability for any actions taken or not taken based on the contents of this blog. The use or interpretation of this information is solely at your discretion. For full guidance, consult with qualified professionals in the relevant fields.